Evidence-first evaluation

Reviewers can assess how each decision connects to source records, rule checks, notices, and internal approval history.

Accrella reviews

A clear diligence page for teams evaluating Accrella. Public testimonials are published only with consent; until then, this page shows what operators, counsel, and accredited LP reviewers should inspect before requesting access.

Accrella reviews should evaluate whether the workbench can prove what source was used, why a lien was acquired or skipped, what notices were produced, who reviewed the file, and how the certificate resolved.

Reviewers can assess how each decision connects to source records, rule checks, notices, and internal approval history.

The product surface is built around county supply, underwriting, servicing, attorney queues, and investor reporting.

Accrella avoids passive-income framing, guaranteed-return claims, and unsupported coverage statements.

01

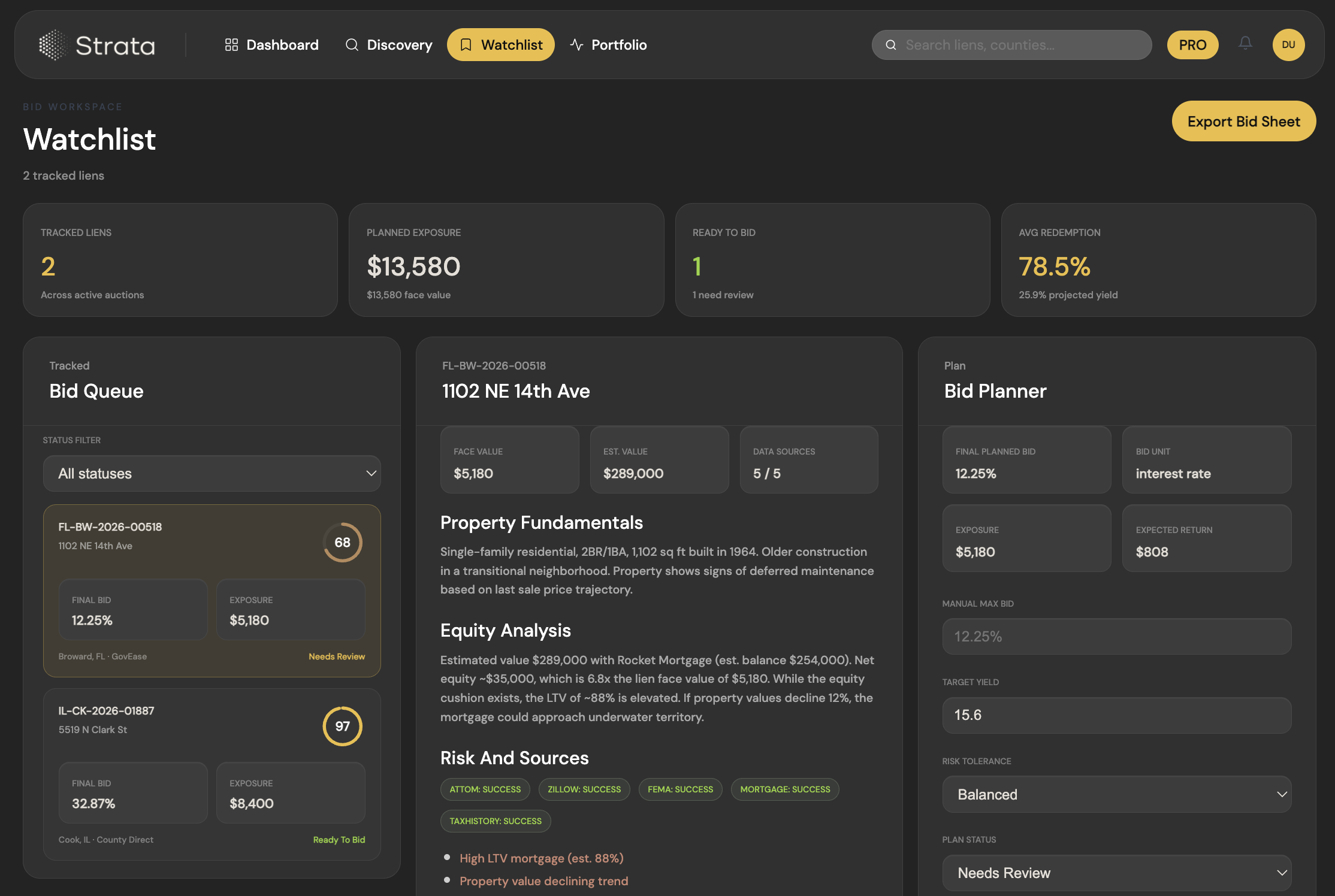

A useful review should test the parts of tax-certificate operations that are expensive to reconstruct later.

Look for source-backed rule fields, freshness signals, registration status, and county-specific operating limits.

Confirm that scoring, hard skips, reserves, and reviewer overrides leave a reproducible decision trail.

Check whether notices, mail evidence, redemption events, disputes, and releases stay tied to the certificate record.

02

Accrella is careful about testimonials because the market is regulated and narrow.

Named quotes should appear only after written consent and conflict review.

Feedback from attorneys, tax-certificate buyers, and county-adjacent reviewers is best summarized by workflow area.

Screenshots, sample evidence packs, and route-level disclosures are stronger than generic star ratings.

Information on this page is product and diligence context only. It is not investment, legal, or tax advice and is not an offer to sell securities.