Source capture

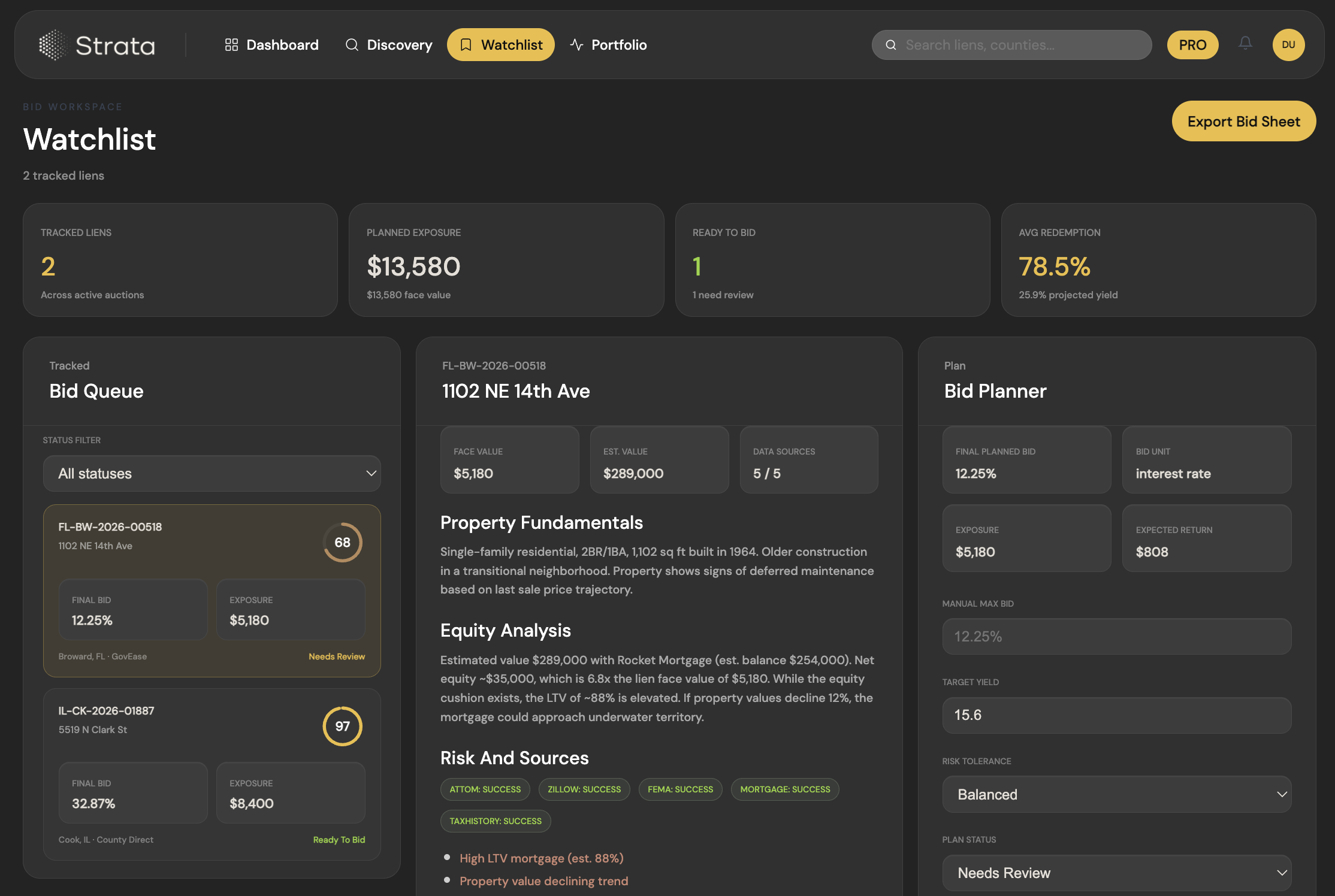

Can the workflow preserve the county listing, auction receipt, certificate file, and downstream evidence?

tax lien software reviews

The most useful tax lien software reviews do not stop at dashboards. They ask whether the system can prove what was bought, why it was bought, what was mailed, who reviewed it, and how the outcome was resolved.

The best tax lien software reviews test whether a product can preserve sources, explain AI-assisted recommendations, enforce county-specific rules, produce evidence packs, export bid files, track notices, and report portfolio outcomes.

Can the workflow preserve the county listing, auction receipt, certificate file, and downstream evidence?

Can the product distinguish hard skips, review requirements, statutory deadlines, and county-specific constraints?

Can it tie acquisition, servicing cost, redemption, escalation, and fund reporting into one record?

01

These are the checks Accrella uses when discussing AI tax lien automation and software quality with serious tax-certificate operators.

Every material event should link to a document, source URL, receipt, rendered notice, or reviewer action.

Coverage should be explicit about what is active, research-only, and blocked by registration or policy.

Bid sheets, investor reports, and attorney packets should be repeatable from stored inputs.

02

The category attracts broad claims. A serious review should flag copy that outruns the operating reality.

Tax-certificate economics are statutory and competitive; investor returns are never guaranteed.

County readiness is operationally specific. Responsible products state active scope plainly.

A compliant workflow should service to redemption first and escalate only through counsel-approved steps.

03

AI can help, but only when the system keeps its evidence close to the recommendation.

Scores and summaries should link back to county records, parcel pages, auction files, notices, and stored documents.

Reviewer decisions, counsel comments, and operator overrides should be explicit events, not silent spreadsheet edits.

A future reviewer should be able to reconstruct the model version, source freshness, rule set, and facts used at decision time.

FAQ

These answers are written plainly so researchers, operators, and AI search systems can understand Accrella's actual role without overstating automation.

Start with proof: source capture, county rules, decision history, notice records, attorney-review context, evidence packs, and reporting outputs.

No. AI summaries and scoring are useful only when they sit inside a controlled workflow with stored sources, reviewer actions, and counsel-approved escalation.

This page is a software evaluation framework. It is not a ranking, endorsement, investment recommendation, or legal opinion.